A laid-off employee spends 45 minutes with a friendly benefits advocate. They hang up knowing which plan fits their family and roughly what it should cost. Then they're sitting there with a plan name, a phone number, and still no insurance. The person who just gave them all that advice can't sign them up.

That handoff is where most workforce transition help breaks down. Advice is the easy part. Getting someone covered, on the right plan, inside a deadline, is the part that counts. Whether a vendor can do that second part comes down to one thing: a license.

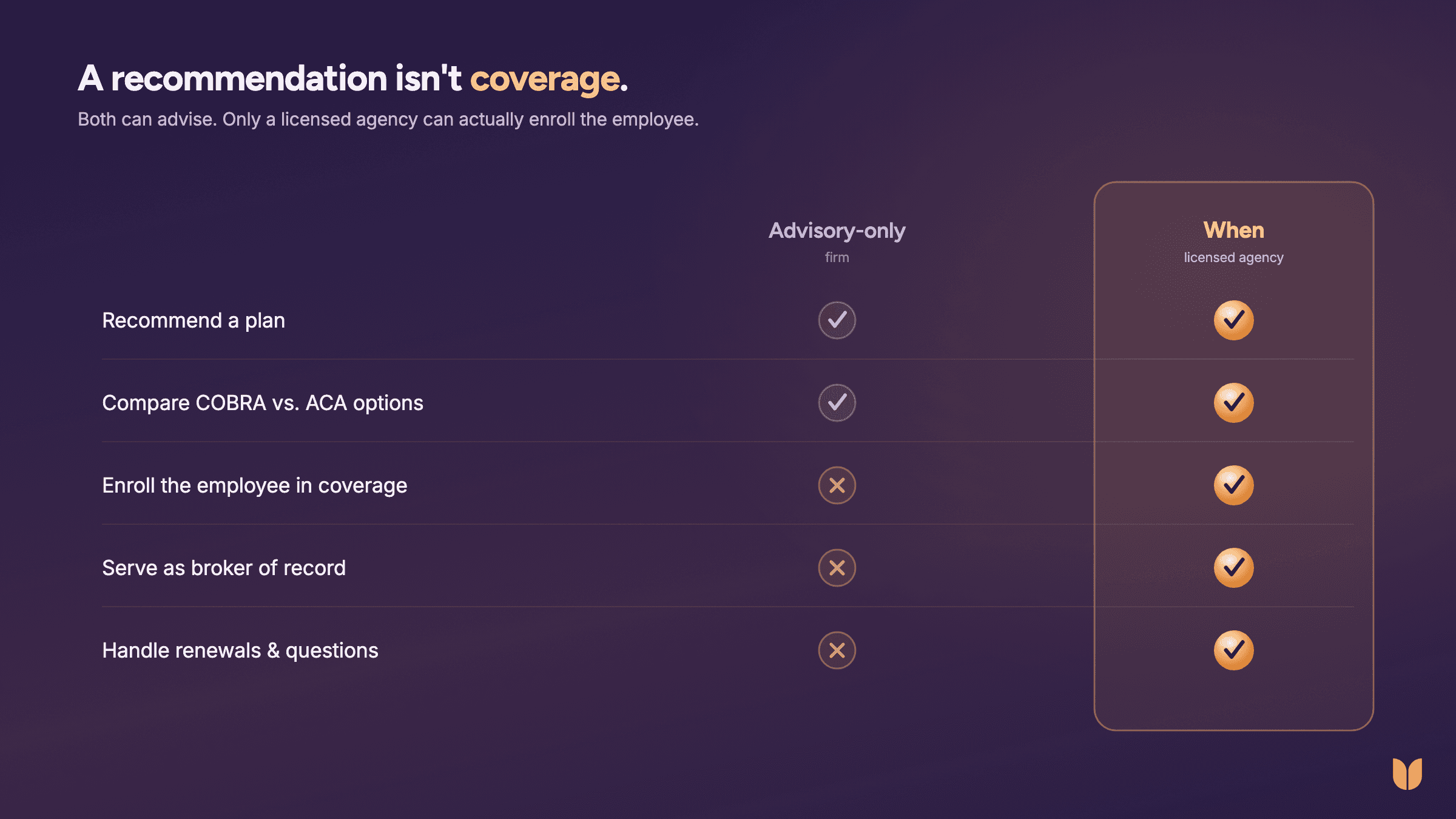

What an advisory service can legally do

There's a clear line in insurance regulation. To sell, solicit, or negotiate insurance, you have to hold a producer license. Every state has adopted some version of the NAIC Producer Licensing Model Act, and the definitions are broad. "Solicit" covers urging someone to apply for a particular kind of coverage. "Negotiate" covers offering advice about the specific benefits, terms, or premiums of a particular policy when you also place that coverage.

Education and advocacy firms stay on the safe side of that line on purpose. They explain how Medicare works, point people toward government programs, and walk through options in general terms. That's genuinely useful, and it's allowed without a license precisely because it stops short of selling anything.

The catch is built into the model. The same boundary that keeps an advisory firm compliant is the reason it can't enroll anyone. It can tell an employee what to do. It can't do it for them. We wrote more about where that line sits for HR teams in What HR Can and Can't Say About Medicare.

Where "unbiased guidance" leaves the employee

Advisory-only firms lean hard on the word "unbiased." The logic: we don't sell anything, so we have nothing to push. Fair enough. But unbiased advice that ends at advice still leaves the employee to handle the hardest part alone.

After a job loss, there's usually a 60-day window to enroll in marketplace coverage. Miss it and the next chance can be months away, with a coverage gap in between. So the employee who got great guidance now has to find the plan again on Healthcare.gov, confirm it's the one that was recommended, check that their doctors are in network, and finish the application before the clock runs out. A lot of people stall right there. The recommendation was free. The follow-through was on them.

Some firms steer people toward Medicaid, disability, or other safety-net programs, which can be the right call in specific cases. For most departing employees, though, the real COBRA alternative is an ACA marketplace plan, and someone still has to enroll them in it.

Why an unlicensed advisory firm is a compliance risk for employers

There's a second reason this belongs on a benefits leader's desk. When an unlicensed firm drifts from general education into recommending specific plans, quoting premiums, and steering enrollment, it edges into activity that requires a license. The model act also bars unlicensed parties from collecting fees tied to the sale or solicitation of insurance. That's a compliance exposure, and it doesn't always stay with the vendor. If a program you sponsor is effectively transacting insurance without a license, that's a risk you've taken on.

A licensed agency removes the question. The activity is permitted, the accountability is clear, and the work product is actual coverage.

When ™ is a licensed insurance agency that enrolls departing employees

We're not an advice line that hands employees back to fend for themselves. When is a licensed insurance agency. Our legal name is literally When Insurance Agency, Inc., we're appointed with major carriers including Cigna, UnitedHealthcare, Aetna, and Blue Cross Blue Shield, and we're a Healthcare.gov partner.

That means we can serve as the broker of record and complete the enrollment. An employee compares COBRA against ACA and private plans, talks it through with a licensed advisor, picks a plan, and enrolls, all in one place. As broker of record, we stay on the policy afterward to handle questions, issues, and renewals. The relationship doesn't end at the recommendation.

One place to compare, decide, and enroll

The practical difference is the number of handoffs. With an advisory service, the employee gets help in one place and then has to go transact somewhere else. With When, comparison, decision, enrollment, and ongoing support live together. Our AI-powered marketplace matches each person to plans that fit their costs, coverage, and doctors, and a licensed advisor is there when they want a human. For older workers leaving the group plan, the same model applies to Medicare.

If you want to see what that looks like against your own headcount and COBRA take rate, run the numbers in our savings calculator or explore the full platform. When you're ready, schedule a demo.

Common questions about licensed vs. advisory-only help

Can an advisory firm enroll employees in health insurance?

No. Selling, soliciting, or negotiating insurance requires a producer license, and education-only firms stay unlicensed on purpose. They'll recommend a plan and explain the tradeoffs, but the employee still has to go enroll themselves somewhere else.

Do you need a licensed broker to offer a COBRA alternative?

To actually get someone covered, yes. A licensed agency can act as broker of record and finish the enrollment, while an advisory service can only hand an employee a plan name and a deadline, not a policy.

What's the risk of using an unlicensed advisory firm?

When an unlicensed firm moves from general education into recommending specific plans, quoting premiums, or steering enrollment, it edges into activity that requires a license. If a program you sponsor is effectively transacting insurance without one, that compliance exposure can land on you as the employer, not just the vendor.

Is When a licensed insurance agency?

Yes. When Insurance Agency, Inc. is a licensed agency appointed with major national carriers and a Healthcare.gov partner, so employees compare plans and enroll in one place rather than getting handed off to finish alone.

If When is a licensed broker, is its advice biased toward higher commissions?

Not when the advisors aren't paid on commission. Ours are salaried, so the plan that fits the employee is the only one we have a reason to recommend. We covered why we built it that way in Why Our Agents Don't Work on Commission.