I talk to HR and benefits leaders at large employers all day. When the topic turns to workforce demographics, it's almost always framed around succession. Who's retiring, who's backfilling, how to hold onto institutional knowledge. Those are real concerns.

But there's a parallel problem sitting in the same data that almost nobody talks about. The moment your employees turn 65, they hit a benefits cliff. And if your organization isn't actively managing that transition, you're the one absorbing the cost.

Let me show you what I mean.

The Scale of the Problem Is Already Here

We're in the middle of what demographers call "Peak 65." More than four million Americans are turning 65 every year right now, and that wave keeps going through at least 2027. The youngest Baby Boomers don't reach 65 until 2029, so this isn't something you can wait out.

At the workforce level, the numbers are striking. Employment of workers 65 and older has more than doubled over the past two decades, according to the Bureau of Labor Statistics. In 2024, nearly 12 million Americans over 65 were still working, roughly 7% of the entire labor force. People are staying in their jobs longer because they want to, and because the math on retirement has changed.

For a self-insured employer with 2,000 or more employees, that means a growing share of your plan members are sitting right at Medicare eligibility, or already past it.

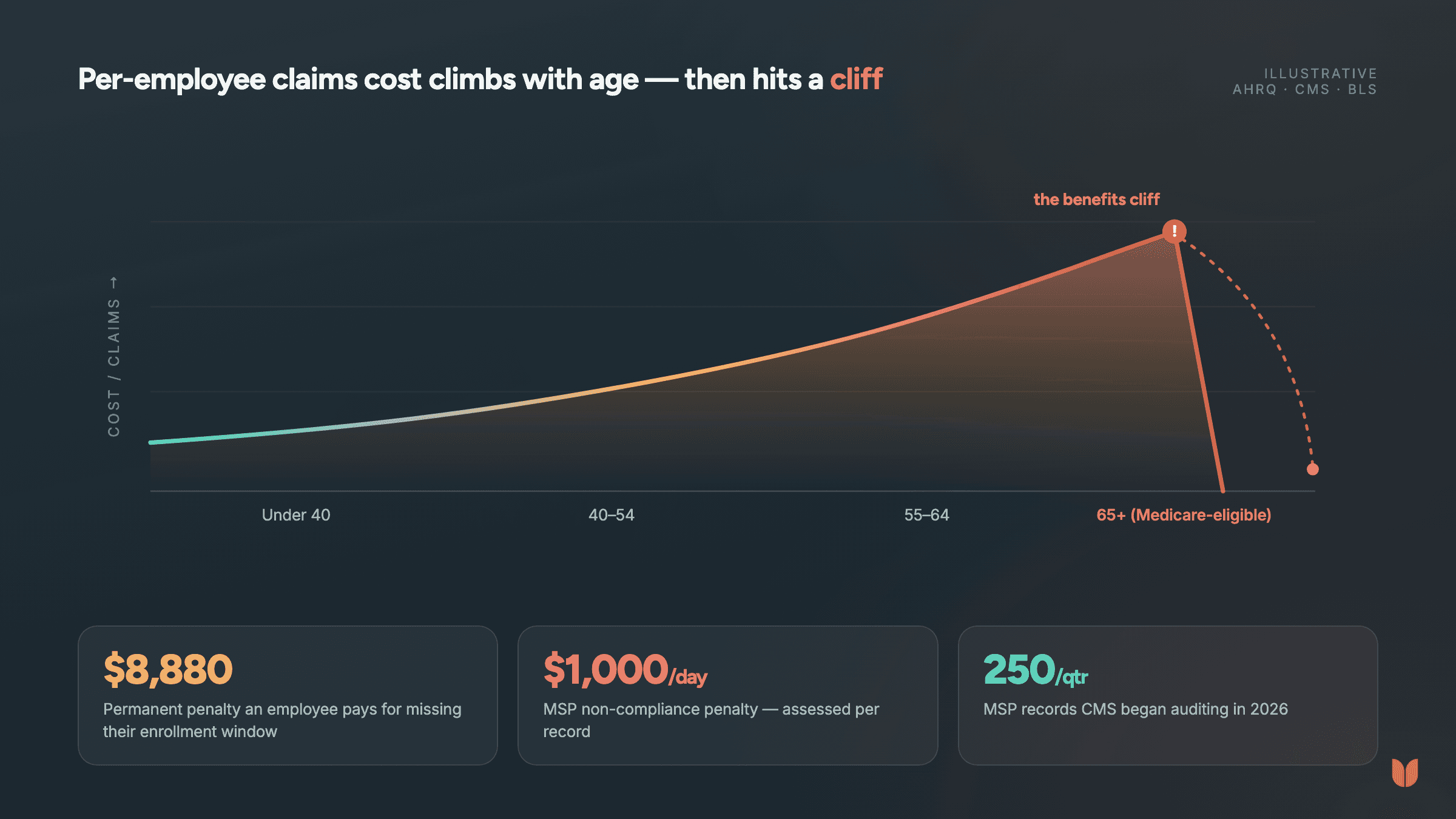

What an Unmanaged Transition Actually Costs

Most benefits conversations stop at succession and miss the real exposure. Here's where it shows up.

Your plan absorbs claims it shouldn't.

For large employers with 20 or more employees, the law is clear. When an active employee is Medicare-eligible, your plan pays first and Medicare pays second. That sounds manageable until you remember that older workers generate substantially higher claims. Research from the Agency for Healthcare Research and Quality found that per-employee premiums at large firms are measurably higher when more of the workforce is over 50. Every month a Medicare-eligible employee stays on your self-insured plan without coordinating benefits is a month you're probably absorbing costs Medicare could be covering. Our Medicare transition support helps employers spot these employees and act before the costs pile up.

Your employees pay a permanent penalty for missing their window.

Medicare has strict enrollment periods, and the penalties for missing them aren't minor or temporary. They're permanent. A Part B late enrollment penalty adds 10% to someone's monthly premium for every 12-month period they were eligible but didn't sign up. At 2026 rates, two years of delay means paying roughly $8,880 extra over a 20-year retirement. That's not a paperwork problem. That's real financial harm to someone who worked for you for decades and trusted your benefits team to help them through it. It's the same thing we wrote about in Americans Are Rationing Medicine to Afford Health Care. The cost of doing nothing lands on the employee, not the plan.

Your organization faces compliance exposure.

The Medicare Secondary Payer rules are getting more teeth. Starting in 2026, CMS began auditing 250 MSP records per quarter, a big jump in enforcement. Penalties for noncompliance can run past $1,000 per day per record. For self-insured plans with large claim volumes, even small reporting gaps add up fast. Employers also can't incentivize Medicare-eligible active employees to drop employer coverage. That rule exists precisely because employers would rather move those high-cost members off the plan.

The COBRA Trap Makes It Worse

There's a related landmine worth calling out: COBRA.

When someone loses active employment, a lot of people instinctively elect COBRA while they figure out their next move. What most of them don't realize, and what too few employers explain clearly, is that COBRA doesn't count as creditable coverage for Medicare. So an employee who spends their COBRA months assuming the Medicare clock is paused will blow past their Special Enrollment Period and trigger the same permanent penalties I described above.

The employee gets stuck with a lifelong consequence. And if the company never made this clear at offboarding, that's a relationship and reputational hit that won't show up on any benefits dashboard. If you're wondering whether your own plan design is feeding this, the question we asked in Our Plan Is Too Rich. They'll Always Choose COBRA. is worth a read.

The Demographic Pressure Is Accelerating

Here's the forward-looking data that should matter to anyone planning for 2026 and beyond.

By 2029, one in five Americans will be 65 or older. By 2032, the country is projected to hit the largest labor shortage in its history, a direct result of the gap between workers and retirees continuing to widen. Organizations with older workforces are already living this. Census Bureau research found that some firms have 25 to 50 percent of their workforce over traditional retirement age, well above the national average, and those companies face compounding risk as the demographics shift.

The cost pressure on self-insured plans is just as clear. Large employer hospital prices have climbed from roughly 10% above Medicare rates in 2005 to more than 100% above Medicare in many markets today. That gap matters a lot when you're deciding whether to help your Medicare-eligible employees make a well-timed transition or keep absorbing their claims at commercial rates indefinitely. Our savings calculator can help you put a real number on that exposure for your own workforce.

This Is Solvable. It Takes Intention.

The good news: managed Medicare transitions aren't complicated. They take two things large employers are completely capable of delivering. Proactive communication and expert guidance, offered at the right moment.

Employees need to understand:

The 7-month Initial Enrollment Period around their 65th birthday

How their employer plan coordinates with Medicare while they're still active

What changes when they retire or lose active status, and why COBRA isn't a safe harbor

The difference between legitimately delaying Medicare and triggering a lifelong penalty

When that guidance lands clearly, and early enough to act on, employees make better decisions, plans avoid unnecessary exposure, and the organization actually delivers on its duty of care to people working through one of the most complicated financial transitions of their lives.

At When, we built our Medicare transition support around exactly this problem. We help self-insured employers systematically find employees approaching 65, give them clear guidance through a dedicated education hub and licensed Medicare advisors, and make sure they reach Medicare with their coverage intact and their choices understood.

The workforce data is telling you this is coming. The only question is whether your benefits strategy is ready for it.

See how When helps large, self-insured employers manage aging workforce transitions.