Captives have built sophisticated machinery around managing risk for active plan members. Chronic condition programs. Narrow networks. PBM contracting. Stop-loss layering. Predictive analytics on the active population. The work is genuinely good, and the best-performing captives reflect it. Top single-parent captives can return 60% or more of stop-loss premium to the owner each year.

But there’s a moment in the employee lifecycle where none of that infrastructure is engaged: the day someone leaves the plan.

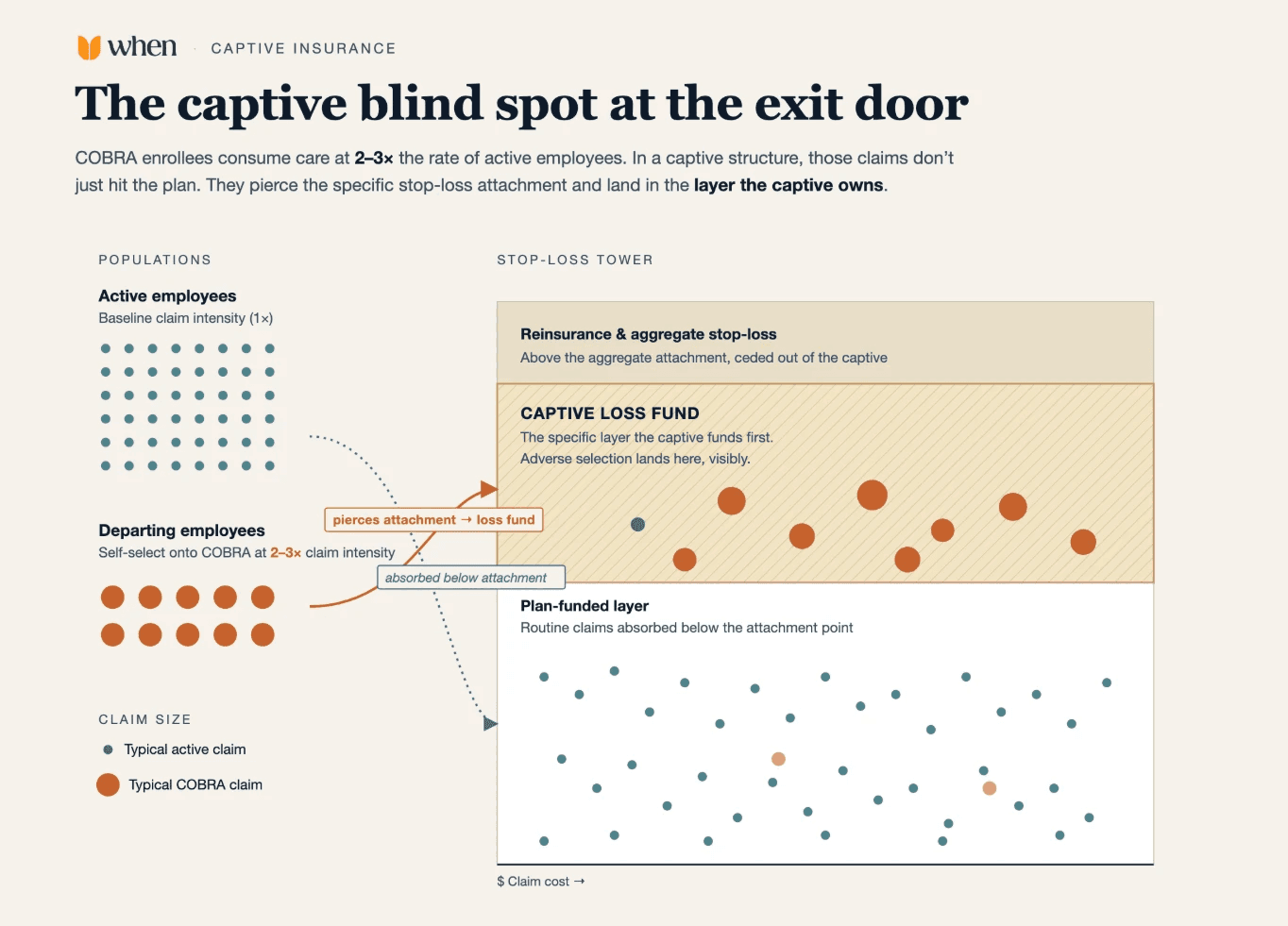

That’s the blind spot. And it’s expensive.

The cost differential captives can’t ignore

COBRA enrollees consume healthcare at roughly three to four times the rate of active employees. This isn’t a controversial number. It’s the entire actuarial reason COBRA premiums are priced at 102% of group cost despite recovering far more than 102% of group claims. The people who elect COBRA are, almost by definition, the people who can least afford to lose coverage: those mid-treatment, those managing chronic conditions, those approaching a scheduled procedure, those who’ve already met their deductible for the year.

For a fully insured employer, this is the carrier’s problem. For a self-funded employer outside a captive, it’s a line item that flows through claims experience and eventually into the next renewal.

For a captive, it’s something different. COBRA claims don’t just hit the plan, they hit the layer of risk the captive owns. A claim that crosses the specific stop-loss attachment point is a claim the captive funds first. The same adverse selection that quietly drags down a fully insured group’s loss ratio shows up much more visibly in a captive’s loss fund.

Group captive or single parent: the ROI flows differently

The captive industry isn’t one structure, and the case for managing COBRA adverse selection looks different depending on which model you’re in.

In a group captive, where dozens or hundreds of self-funded employers share a risk pool, the program manager has leverage most consultants don’t. Solutions that reduce high-cost claims across the membership can be evaluated, endorsed, or built directly into the program — which both improves pool performance and reduces the reinsurance and aggregate stop-loss costs that everyone shares. Return of premium at the pool level tends to be modest in absolute terms, but every dollar of avoided adverse selection improves it.

In a single-parent captive structure, where each self-funded employer owns their own captive and is the first payer of their own stop-loss claims, the math is more direct. Adverse selection avoided is captive premium retained. There’s no risk pool to subsidize, no other members to share the upside with. The single most controllable variable left for many top-performing captives in this structure is the cost of departing employees.

In either structure, the conclusion is the same: COBRA adverse selection is one of the few remaining unmanaged levers in captive performance.

What’s actually happening at separation today

Most captive members have a COBRA administrator. That administrator’s job — and the job they’re paid to do — is to manage compliance. Notices go out on time. Elections get tracked. Premiums get collected. None of that is wrong, and none of it is going to change the captive’s loss fund.

What’s missing is the conversation that happens before the COBRA election package arrives in someone’s mailbox. A departing employee who’s eligible for a spouse’s plan, a parent’s plan (if they’re under 26), a marketplace plan with a subsidy, Medicare, or a short-term bridge to their next job’s coverage will almost always find one of those options more affordable than COBRA — if anyone tells them the options exist. Most never hear it. They get the COBRA notice, they panic, and they elect.

The result is exactly what the actuarial math predicts: the people with the highest expected claims are disproportionately the ones who stay on the plan after they’ve left the company.

Where captives have leverage

The structural advantage a captive has over a standalone self-funded employer is the ability to act once and benefit many times. A group captive that builds a COBRA alternative into the program protects every member’s loss fund without each member having to procure independently. A single-parent captive that adopts the same approach captures the upside directly in its own results.

The data infrastructure is already there. The same eligibility and qualifying-event file that flows to the COBRA administrator is the same data needed to engage a departing employee with their actual options. Implementation isn’t a heavy lift…it’s a reroute.

For the captive consultants advising in both structures, the case worth bringing to the table isn’t a vendor pitch. It’s a structural argument: the cost of doing nothing is showing up in the loss fund every quarter, and the math gets better the larger and more captive-native the implementation.

A conversation worth having

The question for captive managers, owners, and the consultants who advise them isn’t whether COBRA alternatives exist. They do, and the regulatory framework around employer-sponsored guidance into ACA marketplace coverage, Medicare, and other paths has matured.

The question is whether the captive, the structure that already owns the risk on the other side of the exit door, is the right place to make sure those alternatives are being offered.

For most captives, it is.

Talk to When about a partnership

When ™ partners with captives, captive managers, and their consultants to embed COBRA alternatives into the way risk is managed, not bolted onto it. Our AI-powered platform integrates with the same eligibility and qualifying-event data your COBRA administrator already receives, reaches departing employees before the COBRA election package arrives, and walks them through every coverage option they actually qualify for: marketplace, spousal, parental, Medicare, short-term bridge, or COBRA when it’s genuinely the right answer.

The result is fewer high-cost COBRA enrollments, fewer stop-loss claims sourced from the exit door, and a measurable improvement in captive performance.

If you manage a captive program, advise one, or own a self-funded plan inside one, we’d like to talk about what a partnership could look like in your structure. Contact our sales team to learn more today.