Most cost-containment decisions start with the health plan report. HR and benefits leaders scan the highest-spend categories and prioritize the solutions that target them. It’s a rational way to triage a long list, but it quietly works against the move that would help most.

The biggest cost on your plan may be the one you can’t see

Start with what the report doesn’t tell you. COBRA claims usually aren’t broken out as COBRA; they’re absorbed into the plan’s overall numbers. So the cost of your departing population — which runs high, because the people who hold onto coverage tend to be the ones using it — is effectively invisible on the report you’re prioritizing from. If COBRA showed up as its own line item, it would change a lot of conversations.

Then there’s the flip side. The solutions that map to the visible big-spend categories are usually the hardest to put in place. They ask for plan-design changes, carrier integrations, sometimes outright disruption to your health plan. And every one of those pushes the path to ROI out by quarters, occasionally years.

So the highest-impact move gets deprioritized twice: once because it doesn’t show up clearly on the report, and again because the things that do show up are painful to act on.

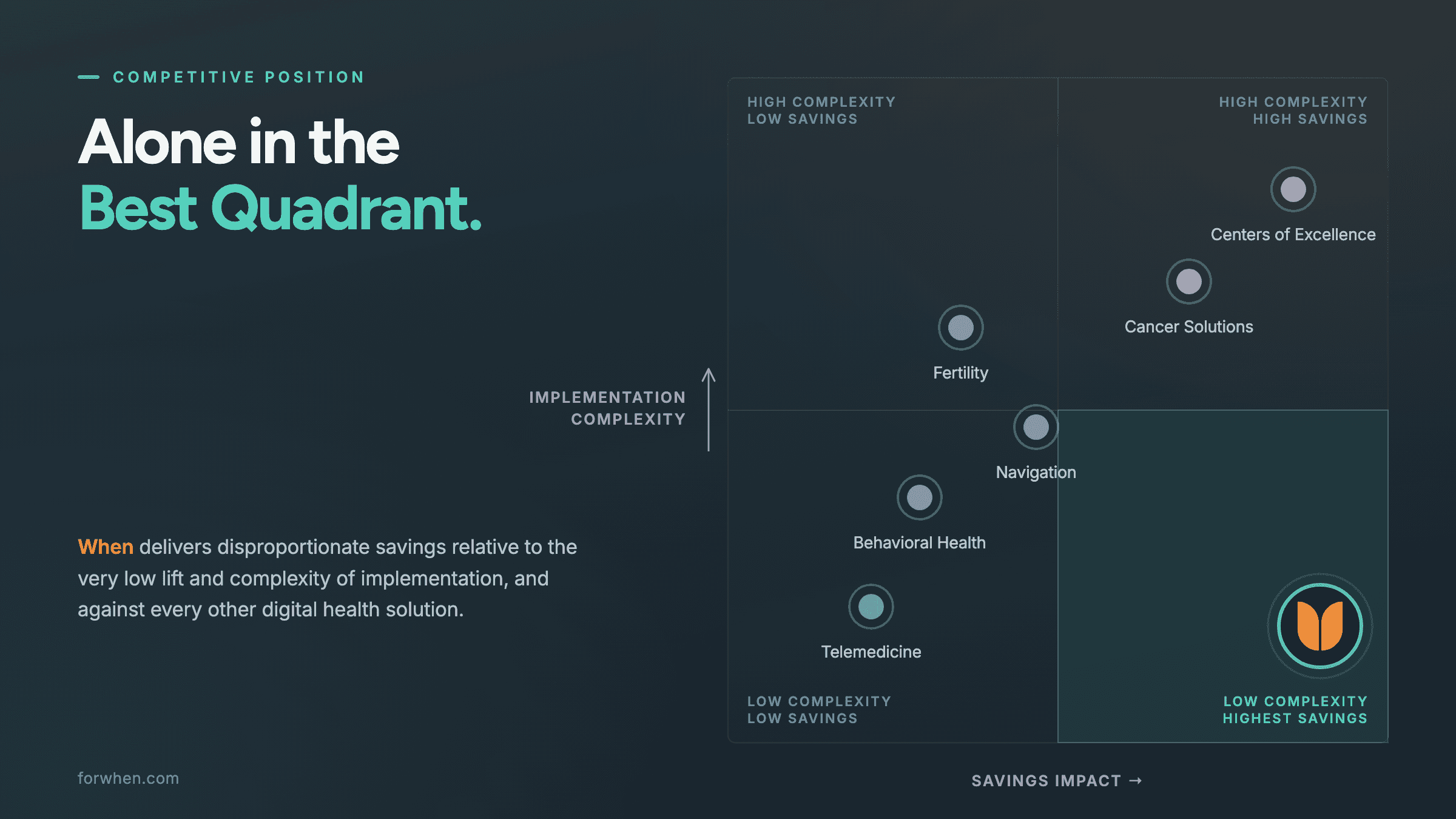

You shouldn’t have to choose between savings and simplicity

When we mapped where the major digital health categories land — savings impact on one axis, implementation complexity on the other — almost everything clustered where you’d expect. Centers of Excellence and cancer solutions can deliver strong savings, but only after months of implementation. Navigation, behavioral health, and fertility sit in the middle: meaningful benefits, with a lift that doesn’t always match the return.

When ™ sits alone in the bottom-right corner: higher savings than any other digital health solution we’ve seen in the market, with the lowest implementation burden in the category. That pairing is the entire argument.

So when “competing priorities” is the reason a rollout keeps sliding, it’s a fair question to put back on the table:

“If When saves more and goes live faster than anything else you’re weighing, why isn’t it at the top of the list?”

When

What When ™ actually does

If you’re newer to us: When ™ helps people make confident coverage decisions during the transitions that tend to cost your plan the most, and we guide each person to the option that genuinely fits them.

The clearest savings shows up at offboarding. When a departing employee defaults to COBRA, your plan holds onto one of its most expensive members, AND who will be 300% more expensive than an active employee. When ™ steps in at that moment with proactive, human guidance, showing each person exactly what COBRA costs against the alternatives they qualify for, and helping them enroll in the right one.

That’s especially decisive for departing employees who are 65 or older. Someone Medicare-eligible who’s facing a COBRA decision should, in nearly every case, enroll in Medicare instead. It’s the better outcome for them and far less costly for your plan. Catching those cases at the moment of transition is where the real claims savings live.

A second benefit your HR team will feel

There’s a related place When ™ helps that has nothing to do with claims. It deserves to be described on its own terms, because the value is genuinely different.

Your active employees approaching 65 have real questions about Medicare: how it works, when to enroll, how it fits with the coverage they already have. Most HR teams aren’t staffed or trained to answer those questions well, and the gap is sharpest at large employers with a meaningful share of the workforce heading toward retirement. When ™ fills it, proactively educating those employees so they understand their options, and so your HR team isn’t fielding questions it was never resourced to handle.

To be clear about what this is and isn’t: it’s a support and experience benefit for your people, not a claims-savings play. Employees who are offered group coverage rarely leave it for Medicare, and we don’t pretend otherwise. The payoff here is a better-served workforce and an HR team that looks buttoned-up on a subject employees genuinely worry about.

What does it actually take to implement When ™?

Here’s the part that tends to surprise people: When ™ isn’t your COBRA administrator, and we’re not here to replace the one you have. We run alongside it.

That distinction is the whole reason implementation is so light. We’re not touching your COBRA process, your carrier, your plan design, or your active-employee benefits. There’s no system for your team to learn and no open enrollment window to wait for.

What we need is the same information you already produce for your COBRA administrator: your Summary of Benefits and Coverage (SBCs) and your employer and employee premium rates. You send us the same file you’re already generating. That’s the lift.

From there, we connect to your HRIS — Workday, Paycom, HiBob, Paylocity, and others are supported — through an API or a secure file transfer. That single connection is all it takes for us to know when someone is leaving and when an employee is approaching Medicare age. We test it end to end, confirm everything works, and go live.

Typical timeline: 2 to 4 weeks, but we’ve done it in less than 1.

Why this matters beyond the spreadsheet

Leaving a job and turning 65 are two of the most disorienting moments in a person’s financial life, and the coverage decisions that come with them are high-stakes and genuinely confusing. The reason to make this easy isn’t only operational, it’s that the people behind those census rows deserve a clear, unhurried path to the right coverage.

So the win compounds. Your team carries almost no lift. Your people get a better, less stressful transition. And the savings you modeled begin accumulating immediately, because nothing stalled the project.

If you want to pressure-test the savings side of that math, our COBRA Savings Calculator is a fast place to start, and our Medicare guidance walks through how that side works. If renewal strategy is on your mind, The Two Levers That Actually Move the Number breaks down where the real leverage is.

See how fast When ™ can go live

The solution you can implement the fastest is usually the one that actually gets implemented. If cost containment is on your roadmap and you’ve held off because the lift looked too heavy, this is the one to look at first.