The compliance line most benefits teams don’t realize they’re walking.

Every week, somewhere in America, an HR professional sits across from a departing employee — someone in their late 50s or early 60s, maybe facing their first gap in employer coverage — and tries to help. They pull up Medicare.gov, walk through the parts, explain the enrollment windows. They’re being generous with their time and knowledge.

They’re also, in many cases, giving unlicensed insurance guidance without realizing it.

This isn’t about bad intent. It’s about a line that’s genuinely hard to see until someone points it out. I’ve worked with benefits and total rewards teams at companies of every size, and this comes up more than almost any other issue in offboarding. HR leaders want to do right by their people. Medicare is complicated. And the instinct to explain things is exactly what makes great HR professionals great.

But Medicare operates under a specific regulatory framework — the CMS Medicare Marketing Guidelines — that draws a firm line between education and advice. Understanding where that line sits isn’t just a compliance exercise. It protects your team, protects your company, and ultimately protects the employees you’re trying to help.

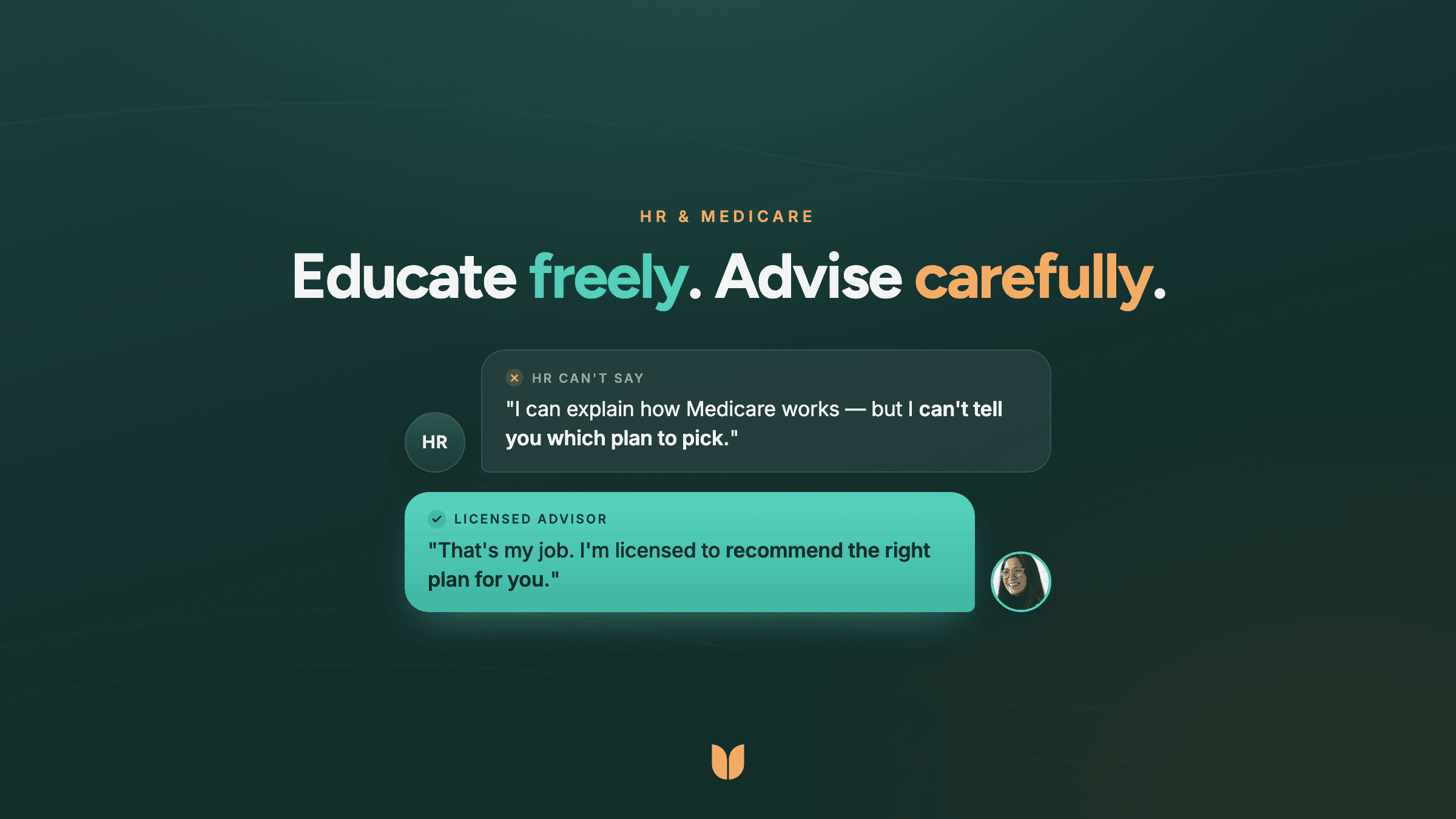

The Line CMS Draws: Education vs. Advice

Under CMS rules, anyone who goes beyond general Medicare education and begins making recommendations about specific plans, coverage types, or enrollment decisions is operating in territory that requires a license.

Education looks like this:

Explaining that Medicare has four parts (A, B, C, D) and what each covers in general terms

Describing when Medicare eligibility typically begins

Noting that there are enrollment windows and that missing them can have consequences

Pointing someone toward Medicare.gov or 1-800-MEDICARE as a starting point

Advice — the kind that requires a license — looks like this:

Recommending whether an employee should choose Original Medicare or Medicare Advantage

Suggesting a specific supplement (Medigap) plan or carrier

Telling someone whether they should delay Part B enrollment based on their situation

Opining on whether COBRA or Medicare is the better choice for a specific person

The challenge is that these two categories don’t always feel different in the moment. An employee asks, “Should I go with a Medicare Advantage plan or stick with Original Medicare?” and the instinct is to answer. But that question, in that specific form, is a licensed insurance question.

Why “Just Go to Medicare.gov” Creates Its Own Risk

A common fallback — and one I hear often — is to redirect employees to Medicare.gov and leave it there. It feels responsible. It’s not wrong, exactly. But it creates a different kind of risk that benefits teams often overlook.

This situation comes up in two very different contexts, and both matter.

The first is proactive: an employee is approaching 65 and aging into Medicare eligibility while still on your plan. They may not have initiated this conversation — you’re bringing it to them. Done right, this is one of the most meaningful things a benefits team can do. Medicare eligibility doesn’t pause because someone still has employer coverage, and the decisions they make in this window — about whether and when to transition off the group plan, how to coordinate benefits, when to enroll in Part B — have long-term financial consequences. These employees need guidance, not just a URL.

The second is reactive: an employee is leaving the company, voluntarily or not, and suddenly faces a coverage decision on a deadline. For someone Medicare-eligible, that means weighing COBRA continuation against Medicare enrollment — two systems with different costs, different rules, and a hard timeline for each. The wrong choice, or a delayed one, can mean permanent penalties or a gap in coverage during exactly the kind of life disruption that makes continuous coverage most important.

In both cases, Medicare.gov is comprehensive and accurate. It is not designed for someone trying to navigate either of those situations in real time. The site won’t ask about their spouse’s employer coverage, flag the interaction between their HSA and Medicare enrollment timing, or help them model the true cost of COBRA versus making the Medicare switch now. When an employee comes back to HR with follow-up questions — and they will — the conversation picks up exactly where it left off, except now it’s more specific, more personal, and more squarely in licensed territory.

Pointing someone toward a resource isn’t the same as making sure they’re taken care of. And for employees at this crossroads, the stakes of a misstep are real: late enrollment penalties on Part B are permanent, calculated as a 10% premium increase for every 12-month period they were eligible but didn’t enroll. That’s not a recoverable situation.

What Unlicensed Guidance Actually Costs

The exposure here is real, even if enforcement against individual HR professionals is rare. The more immediate risks are:

Liability for the employer.

If an employee later claims they made a Medicare decision based on guidance from HR — and that decision resulted in a coverage gap, a penalty, or a wrong plan choice — the company can be drawn into that dispute. Benefits conversations during offboarding are often documented, and HR teams are increasingly on record via email and offboarding portals.

Harm to the employee.

This is the one that should matter most to anyone in HR. Medicare decisions made on incomplete or incorrect information can follow someone for years. Permanent penalties. Coverage gaps during a health event. A Medigap plan that doesn’t work with their preferred doctors. These aren’t abstract risks — they’re the real-life consequences of advice given without the training and licensure to give it well.

How Benefits Teams Can Stay in Bounds

The answer isn’t to stop caring about employees who are approaching Medicare. It’s to structure the support so that the right people are doing the right parts of it.

Here’s a framework that works:

HR’s job:

Inform employees that Medicare is a consideration at this life stage, explain the general timeline and the importance of not missing enrollment windows, and connect them with a licensed resource before they make any decisions.

A licensed professional’s job:

Everything else. Scope of appointment, plan comparison, enrollment support, coordination with employer coverage, penalties analysis — all of it.

When uses this model intentionally. Our licensed advisors handle the Medicare conversations that require a license — both the proactive aging-in journey and the reactive offboarding moment. Benefits teams using When can have confident, caring conversations with employees about what’s ahead without stepping into the territory that creates risk for them or their company.

That’s not HR abdicating responsibility. It’s HR doing its job well — knowing where its expertise ends and directing people toward the right expertise for what comes next.

A Quick Reference for Benefits Teams

When you’re in a conversation with a Medicare-eligible employee — whether you’re proactively guiding them toward eligibility or supporting them through a departure — here’s a simple way to think about it:

Safe to say:

"Medicare eligibility generally starts at 65, and enrollment timing matters — there can be permanent penalties for missing the window."

"Whether or how Medicare interacts with your current coverage is something a licensed Medicare counselor can walk you through."

"We’ve connected you with a resource that specializes in exactly this kind of transition."

Not safe to say:

"Medicare Advantage is usually the better deal."

"You probably don’t need a Medigap plan if you’re healthy."

"I’d skip COBRA and just go straight to Medicare."

"Most people in your situation do X."

If you’re not sure which side of the line a statement falls on, the rule is simple: if it’s a recommendation specific to this person’s situation, it needs a license behind it.

The Real Risk Isn’t Malicious. That’s What Makes It Hard.

Benefits and total rewards leaders I work with are, without exception, trying to do right by their people. The Medicare compliance issue isn’t a story about negligence — it’s a story about a regulatory framework that most HR professionals were never trained on, applied to conversations that feel like basic human helpfulness.

The fix isn’t to become a Medicare expert. It’s to understand enough to know where to hand off — and to have a trusted, licensed resource ready when you do.

That’s what protecting your team actually looks like.

When helps employers support employees through health coverage transitions — including Medicare — without putting HR in an unlicensed advice position.